Insurance for Superyacht Crew – Your Financial Lifejacket

Are you wearing your lifejacket? You probably aren’t. But you do have one and you also know where it is in case you need it. They are part of the job and of life at sea.

You probably don’t give your lifejacket much thought. It’s there for emergencies and that’s great. You’re not sure you’ll ever need it and you’re hoping you never will. But if you ever do, it may literally save your life.

So if we asked you if you would like to have a lifejacket on board? You’d probably say yes.

You’d answer the same if we asked about the boat’s fire-suppression and firefighting equipment. Would you serve on a superyacht that didn’t have any?

Of course you wouldn’t. The sea is not a place for the unprepared. You’re a professional, you know that and you take precautions. The consequences of not having lifesaving and firefighting equipment on board when you need them could be catastrophic.

You might not need them, but it brings huge peace of mind, in case you do.

Yet while having adequate protection on a journey at sea is a no-brainer for everyone, having adequate protection on the journey of life is something most people don’t give a second thought to. Superyacht crew included.

What happens if you fall ill or are injured? What if you can’t work for an extended spell or die? These are important considerations. Especially if you’re planning for your future and if you’re building a financial plan. And even more so if you have dependents.

These are very important issues and you need to take control

You might argue that the boat provides medical insurance, and even a bit of life/ disability cover.

Key point: However good the medical cover or life assurance or disability cover on board is, it will only cover you while you are employed on the boat. Once you leave what happens then?

What happens if you fall ill or injured and your recovery takes longer than your employment contract on board the yacht? You could find yourself without health cover from one day to the next. Not only that, you’d be looking to cover the costs of your recovery at a time when you aren’t able to work. Also, you won’t be able to get your own health Insurance at that stage to cover an existing condition.

Bad news: if you rely solely on the insurance offered by the yacht without thoroughly checking the protections it provides you, you might find yourself caught out very badly when you need to call upon it. The protection may be wafer thin.

Good news: by the time you’ve finished this blog post, you’ll be able to take control of your protection.

Health insurance that isn’t good for your health

Insurance is only worthwhile if it gives you the protection you need when you need it.

When it comes to health insurance that means you need to be wary of three things:

- will it give you access to the care you need?

- will it give access to care where you need it?

- will it be valid when you need it?

The first and second considerations are to do with the medical facilities and services you will be able to rely on when something goes wrong with your health or in the event of an injury. You want as wide a range of services included as possible and in as many locations as possible—provided they make sense.

For example, medical care in the US is horrendously expensive. The upside is that every imaginable health solution is available in the US, and at world-beating quality levels. The downside is that it comes with an eye-watering price tag. Don’t be fooled, five- and six-figure medical bills aren’t uncommon in the US. What’s more, if you don’t have insurance and can’t stump up a credit card with sufficient credit limit, you may not get past the admission desk.

So if you have any reason to be in the USA at all, you need solid medical insurance that covers you there. You won’t be surprised to learn that comes with a bump in premium, compared with insurance that doesn’t include the States. As a result, medical insurance often falls into two categories: worldwide and worldwide-excluding-USA.

However the cost of medical care for any serious illness or accident is likely to be huge, wherever it happens.

Does the medical insurance provided by the yacht cover you for visits to anywhere, while you are on leave? You might find you aren’t covered for trips while away from the boat, regardless of where you are going.

On top of which, if you fancy some skydiving or whitewater rafting while on holiday, followed by a bungee jumping marathon, you’ll want to check whether that sort of activity is covered. They often aren’t. Skiing? Ditto. Climbing? … You get the idea. If you’re going to do anything more than drink lattes at museum cafés, you’d better check the fine print.

Income replacement keeps the money coming in

Income replacement is often overlooked by superyacht crew.

Don’t make the same mistake. It is vital.

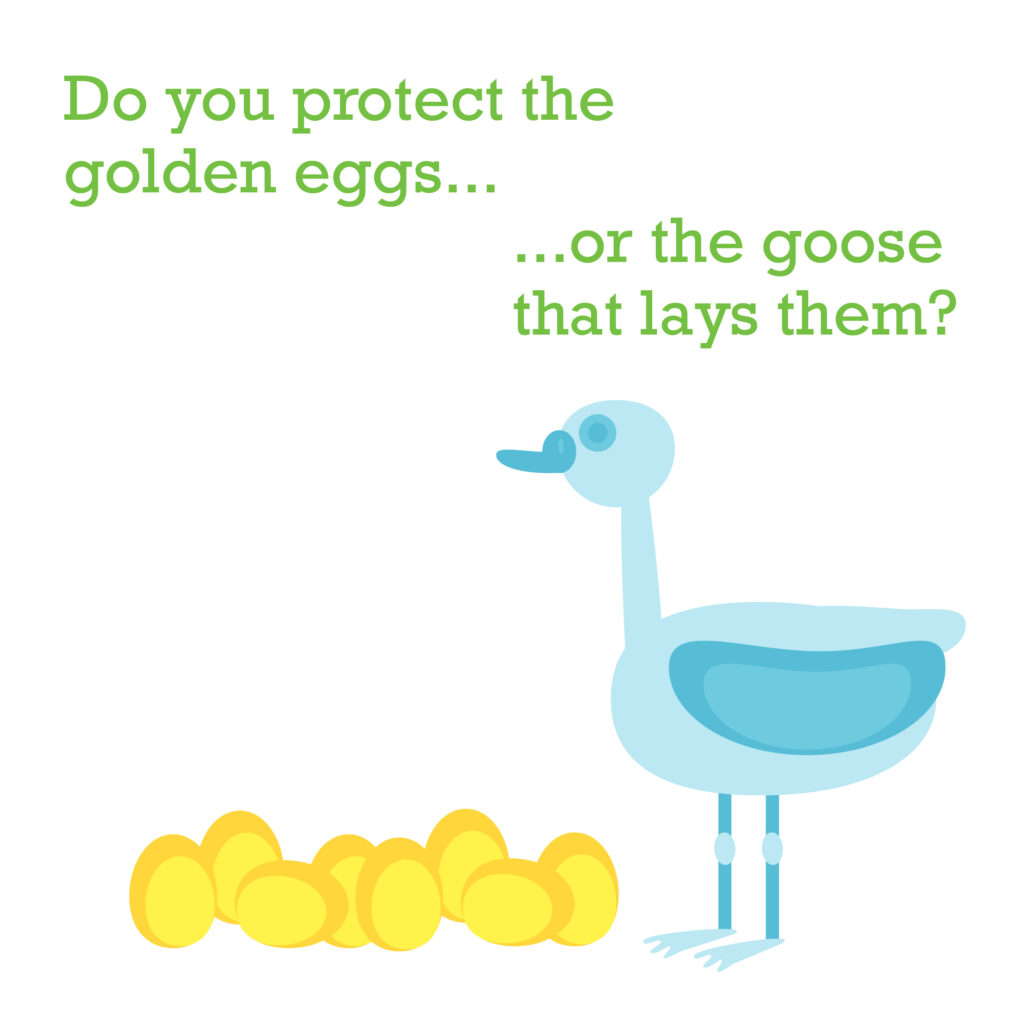

We often ask people this question: if you had a goose that laid golden eggs, would you protect the eggs or the goose?

Nearly everyone gets the answer right. You protect the goose. After all, no more goose, no more golden eggs.

Now… some superyacht crew don’t realise that they are the goose. Or more accurately, their ability to make money is the goose. And if something happens to their ability to lay golden eggs (make money), they won’t be able to afford the lifestyle they’ve become accustomed to. Worse still, if they have dependents (spouse, children, elderly parents), their ability to look after them evaporates if they can’t work due to illness or injury.

Incredibly, even when they do realise this, many superyacht crew shrug their shoulders.

Again, don’t make that mistake.

Protect yourself so that if your ability to lay golden eggs is diminished, you have income replacement insurance that will provide you with an income while you are unable to work.

Typically, income replacement insurance can be set to kick in after a certain period of time. 4 weeks to 13 weeks is a common period. So you may need to make sure you have sufficient funds to cover yourself for the first three months of your recovery from illness or injury.

That’s one of the reasons we tell our clients to have three to six months’ living expenses saved up and set aside somewhere before you even start thinking about investing in medium- or long-term investments. That buffer is key to overcoming temporary glitches in your income, allowing you to continue funding your investments and other life commitments.

Again, we can’t stress this enough if you have dependents.

Life assurance continues your love and support

We also have to raise a grim topic. Especially if you have dependents, it’s really important you take this into consideration.

What happens if the worst happens and you pass on, leaving them behind?

Fortunately, while you aren’t immortal, your ability to provide for your dependents can be.

Doesn’t the boat have to provide you with life assurance, so why bother looking into this yourself?

Yes, under the Maritime Labour Convention, your employer must provide you with life assurance.

Equal to one month’s salary.

One.

Month.

Let’s be frank. That’s as good as useless. If you have dependents who will need support beyond a single month it’s brutally inadequate.

Life assurance falls into the golden goose category, as far as we’re concerned. It’s a no-brainer for any superyacht crew with dependents.

Broadly speaking, there are two flavours of life assurance.

Term life assurance and whole-of-life life assurance.

Term life assurance is like renting life insurance. You have it for a period. For instance, if you have children, you might take out this form of life insurance until they are 21 or maybe a little older. It runs out just as they are able to make their own way in the world. It provides them with money until that time.

Whole-of-life life assurance pays out regardless of when you die. Understandably, this form of life cover is more expensive, because the underwriter knows that they will have to pay out eventually. Sorry, you aren’t going to live forever. But there will absolutely, definitely be a payout on your death.

With term life cover, the underwriter only pays out if you pass away during the term of the cover. Once it lapses, so does their obligation to pay out if you die. Their liability is time limited, so the cover is less expensive.

Other things that impact the prices of life cover include your age, your overall health and health history, any (pre-)existing health problems, your job, your hobbies and spare time activities, and your overall lifestyle.

Insurance stops fate’s worst excesses

Insurance is all about reducing the impact of life’s bumps in the road. Sometimes, those bumps are minor. You barely notice them and get past them easily. Sometimes, though, they are big, dangerous and have a huge impact.

You can’t stop bad things happening in life. They’re the price you pay for being allowed on this ride. But you can protect yourself as best you can from the financial consequences.

Health cover pays for the cost of getting better.

Income replacement insurance keeps the money coming in while you do so.

Life assurance keeps your love and support for your dependents flowing when you are no longer able to.

So here’s a question for you.

Follow-up question: will you protect the goose that lays the golden eggs?