Are Tracker Funds the Answer?

Here’s a popular piece of financial advice: Just invest in a tracker fund.

Simple as that. Put your money in a fund that tracks one of the major stock market indices, like the S&P 500 or the FTSE 100.

Job done.

It’s not terrible advice. Especially compared with doing nothing with your money or, even worse, just spending it all.

But it’s not the best advice.

Let’s look at why. And let’s also consider a better alternative.

Why a tracker fund is not the worst advice

When you invest in a tracker fund, you’re investing in the same basket of stocks that make up these markets.

More likely than not, you’ll be investing money on a monthly basis, which means you’ll be buying stocks at all stages of the market cycle, including when stocks are at low points. That’s exactly when you want to buy, because there is more opportunity for growth and profit.

But timing the market is hard, so spreading your investments like this means you’ll benefit at least some of the time.

Over the course of years and decades, it’s very likely indeed that the value of your investments will increase. Maybe even considerably. After all, while there have been dips, some quite severe, the major stock markets have always recovered and have grown steadily over time.

What more could you possibly want?

Think like the yacht owner

THEY ARE BETTER AT MONEY THAN YOU

If the best route to strong financial health were merely investing in a tracker fund, the superyacht owner would just bung all of their money into one.

Do you think the yacht owner has all of their money in a tracker fund?

Or do you think they have many different types of investments?

It’s the second one, isn’t it?

A tracker fund is not diversified

TRUMP PROVED THIS

You might argue that a tracker fund is diversified. After all, it is made up of the stocks of hundreds of companies traded on a particular exchange.

How much more diversification do you want?

Well, think of each stock is an egg. What you’ve done is put all your eggs in one basket.

If something happens to the basket, you’re in trouble.

Why do you think there was such panic when Trump started taking a sledgehammer to US trade policy, sending the stock markets into turmoil? Because regular investors had their money tied up in tracker funds and suddenly the single market they had their money in took a steep dive.

Overnight people looking to cash in their pension funds found their funds were worth much less.

Do you know who didn’t panic? The superyacht owner. They won’t have been pleased, because they will have some money tied up in stocks, of course. But they won’t have panicked. They didn’t need to.

While everyone else was worried about the state of their single egg basket, the yacht owner took comfort from the fact that they have a big collection of different egg baskets, some of which will have increased in value. Gold and government bonds, for instance.

Also, with the markets at a low, they probably invested more money in stocks to take full benefit of the inevitable market bounce back.

Choppy waves and high winds are OK during the voyage

BUT NOT WHILE YOU’RE TRYING TO DOCK

Volatile markets are fine when you look at them over the long term. They even out, generally in a nice upwards direction.

But there is a moment when you don’t want volatility. That’s when you’re cashing in your funds. Just like US citizens approaching retirement, you don’t the value of your fund to bounce up and down. You want stability.

It’s a bit like taking the yacht across the Atlantic Ocean between seasons. During the voyage, periods of choppy seas and high winds are uncomfortable, but you’ll get through them.

You don’t want those conditions at the end of your voyage, when you’re trying to dock the boat. That’s when you want flat water and a breeze at most.

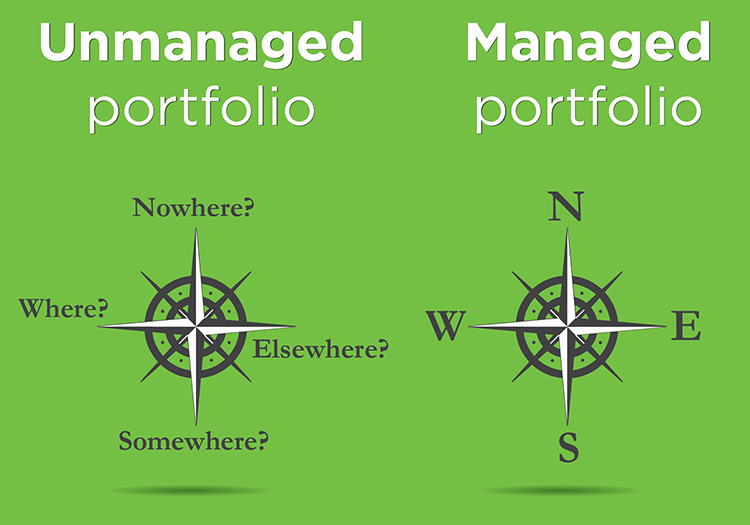

If you simply put your money into a tracker fund, then you’re relying solely on the state of the market when you come to cash in. Who knows what the conditions will be like just at that moment?

Wouldn’t it be better to have already planned to put your money in less volatile investments so that the value of your portfolio is more stable when you want to sell? In other words, having a planned and managed approach to your financial health.

Invest According to a Plan

INSTEAD OF ‘FIRE AND FORGET’

Investing in a tracker fund is a bit like setting sail on a voyage with a rough general direction in mind.

Let’s take the Atlantic Ocean crossing again.

You could set off from Europe, pointing roughly west, in the knowledge that over there on the other side of the ocean is some land you’re bound to reach at some point.

Who knows where you’ll end up and when?

That’s the tracker fund approach.

You’re pretty much guaranteed to reach some sort of a destination, but what it is and when you’ll get there are unknown. It might be the Caribbean. It might be Nova Scotia.

Alternatively, you could pick a destination and plot a course to take you to it, correcting as needs be along the way. Your destination, route and date of arrival are known.

In other words, you end up where you want to be, when you want to be there.

Again, how do you think the yacht owner manages their money? Fire-and-forget or planned-and-managed?

Experience prevents existential panic

WOULD YOU STAND ALONE ON THE BRIDGE?

Investing in a tracker fund is like enabling the autopilot on the bridge because you don’t actually know how to sail a superyacht.

You might get away with it. But what happens when things go wrong? You hit a storm, for instance? The autopilot won’t do much for you, and you don’t have the experience to deal with the situation.

There’s a chance you’ll panic.

You might even decide to abandon ship: sell your investment before things get worse.

In doing so, you’ve crystallised your losses and made them real.

When the seas calm, you’ll realise it would have been better to have stayed on the yacht. Now the markets are recovering, you’re missing out on the chance to recover your losses and, most likely, continue benefiting from long-term growth.

The yacht is sailing away over the horizon without you.

When the going gets tough, when the markets have a wobble, when the US President is driven by impulse rather than insight, that’s when you need a calming presence to help you understand what’s going on and respond appropriately.

That’s why newbie deckhands don’t command superyachts. Captains do. They have the experience to sail the boat during difficult times and easy times. They are the calming, knowledgable presence on board.

An alternative to tracker funds

THE ONLY WAY TO ACHIEVE YOUR GOALS

Look, this isn’t going to come as a huge surprise to you.

The best way to invest your money is as part of a coherent financial plan. And your financial plan is in service of your life plan.

Your life plan sets out your medium- or long-term life goals. It describes your destination.

Your financial plan figures out the cost of reaching your destination and plots a course to get you the money you need. It guides your investment decisions.

SHOCK:

As part of a financial plan, you’ll be investing in a tracker fund. Maybe even several.

BUT:

You’ll be investing in a range of other kinds of funds as well. Some of which will be funds of funds. (Eggs of baskets within bigger baskets.)

Early on, you’ll be looking to invest where returns (and risk) are higher. Later on, as you approach your destination, you’ll be dialling down the risk.

All according to the plan.

And when the plan needs adjusting, to manage a big storm, you’ll probably get guidance from the people who helped you make your life and financial plan.

Because just like the superyacht needs a crew to get it safely to a destination, you will benefit from having people you can rely on too.

You could row your way across the Atlantic on your own. But that’s needlessly hard.

Why not let your very own crew help you with the work instead?

(We’re talking about us, in case that wasn’t clear.)

Tracker funds aren’t bad

BUT THEY ARE ONLY A SMALL PIECE OF THE PUZZLE

First and foremost, we’d encourage you to do something with your money. If all you ever do is put money regularly into a tracker fund, you will have done more than 90% of superyacht crew.

But you won’t be making the most of your unique financial opportunity.

You could say, you’d be losing money, because you’re not taking 100% of the financial benefit you could take from your career in yachting.

Being pro-active and hands-on with your money, and managing it according to a plan, will give you a chance of making substantial money from your time in yachting to kickstart the next phase of your life.

Here’s an example of managed money

HEAR CALM PEOPLE TALK CALMLY

The Trump Tariffs have had a massive impact on markets. But what does this mean for investors? We had a call with Glyn Owen and Andrew Hardy of Momentum Global Investment Management to find out.

If you want a level-headed take on the situation, watch the video below.

If you’d like early access to these videos, then sign up to our monthly email newsletter here: Insider Briefing.