Change Your World: Best Practices and Recommendations for Saving for Superyacht Crew

Did you know that superyacht crew have a superpower?

You might not be able to save the world, but you can save money far beyond the abilities of most people. In fact, you can save so much money, you can change your world.

On average, shore-dwellers with a regular 9-to-5 day job are able to save 10% of their income. In other words, if someone earns a salary of €3,000 to €4,000 per month, they are putting €300 to €400 away in savings each month. That’s €3,600 to €4,800 per year.

Even if they have a simple savings account (not the best option) rather than a savings plan (much better), they will have €36,000 to €48,000 saved after 10 years—roughly the same length of time as a solid career in yachting.

Want to hear more? We think you’ll enjoy it.

Your saving superpower in numbers

Let’s say you earn €4,000 per month on board the superyacht. If you’ve been in yachting for a while, your salary may be much higher than this.

Your daily living expenses, such as accommodation, food, clothing, electricity, water, are taken care of and you don’t have to pay for a daily commute to work. So you’re already way ahead of anyone in a regular job ashore.

You may even be in a position where you don’t have to pay income tax, because you don’t spend long enough in one place to fall under its tax rules.

Note: tax is tricky, so make sure you seek expert advice.

We can put you in touch with someone who can help you understand your tax obligations and stay compliant. Click here: Tax Advice for Superyacht Crew

So, your daily living expenses are minimal and you may even be free of income tax obligations.

Let’s say you keep €1,000 per month for yourself to have some fun. Why not? You work hard, you deserve to spend money on yourself.

That would mean you could set aside €3,000 per month in savings.

Now, if you were living and working ashore, you’d have to be earning €30,000 per month (!) to be able to save that amount. Remember, the average ability to save among shore-dwellers is 10% of their monthly income.

Your savings potential is superpowered compared with theirs.

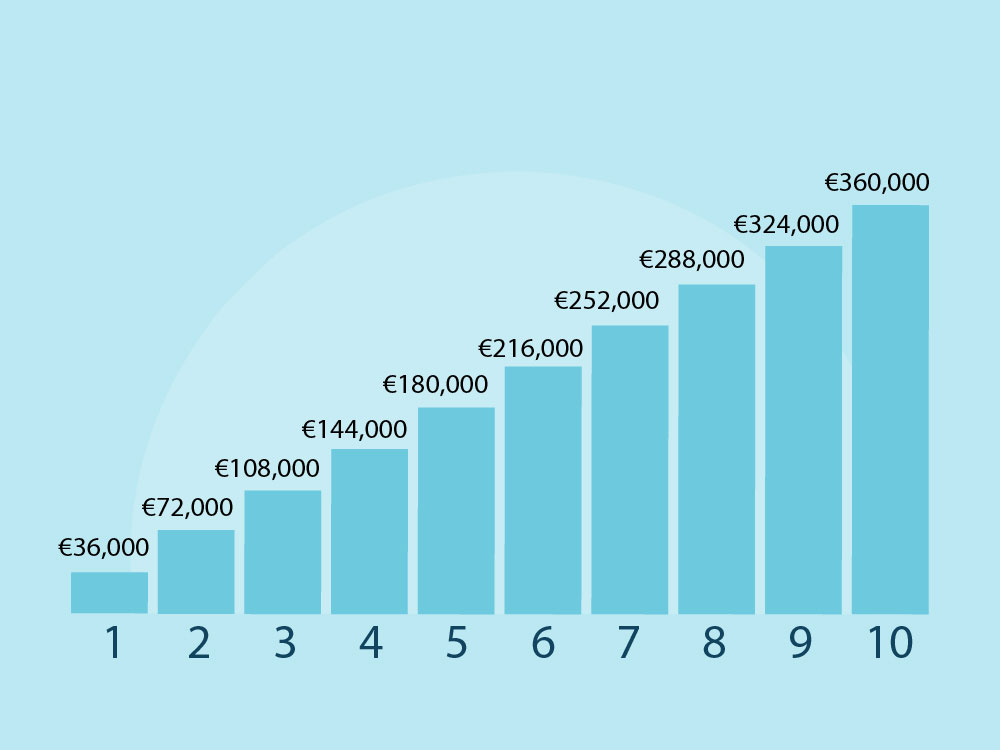

While someone who lives ashore and earns €4,000 would have €4,800 saved at the end of the year, you’d have 12 x €3,000 = €36,000 saved.

Also, they wouldn’t have been able to spend €1,000 per month on themselves to have fun. Their salary gets eaten up by rent/mortgages, food bills, household expenses, utility bills, tax, commuting expenses etc.

And after 10 years, you’d have €360,000. Just by saving.

That’s also assuming you never had a single pay rise in that time—or if you did, you kept your monthly savings amount the same. But you will have had multiple pay rises. And chances are, you will have raised your monthly savings amount.

Also you won’t just put your money into a savings account. That’s wasting your money. Instead, you’ll put it into a savings plan.

A savings account vs a savings plan

Put simply, a savings account is a regular bank account. You have immediate access to your money and you may or may not get some form of interest on your savings. Although, even if you do, the interest rate is likely to be so minimal it probably won’t make up for the inflation rate.

A savings plan is a structured, medium- to long-term savings vehicle that should provide you with a decent return on the money you deposit.

You are committing your money for a period of time, so it’s less accessible at short notice, but in return over time, you should be getting growth on your savings which should more than offset inflation.

Just on that, if you’re not 100% sure about inflation: inflation means your money is worth less over time. In other words, if you buy a basket of goods today for €100 and the annual inflation rate is 3%, you’ll have to pay €103 or so for the same basket of goods next year.

Over a ten- year period, inflation can really affect what you can do with the money you have saved. Placing your money in a savings plan, where your money can grow should offset the impact of inflation. In fact, it could more than offset it by growing your money at a faster rate than inflation. So not only do you beat inflation, you end up with more spending power overall.

Supersizing savings for superyacht crew

Every superhero (that’s you) needs a sidekick.

When it comes to your finances and savings, that sidekick is something called ‘compound growth’. It sounds boring, but just wait until you see what it will do to your money.

Let’s start with a simple example.

Say you put €100 into a savings plan that grows 5% over the year.

At the end of the year, your money has grown from €100 to €105.

At the start of year 2, you put in another €100, so your account is now worth €205.

Don’t forget, if you only had a savings account, you’d have €200 at this stage, because you wouldn’t be getting any growth. But, who cares about a measly €5, right? Hardly worthwhile. Well, read on.

At the end of year 2, your money has grown by 5% again. You now have €215.25. Not only did you get 5% on the money you put in yourself (€200), you also got 5% on the growth you made the year before (that €5). And that was money you didn’t put in. Your sidekick compound growth did that.

At the start of year 3, you put in another €100. At the end of it, you have €331.01, thanks to compound growth. If you only had a 0% savings account, you’d still only have the €300 you’d put in. That’s better than nothing, of course. But the compound growth of a savings plan means you’re over 10% ahead (€31.01).

If you keep this up for ten years, you’d have €1,483.57—having only put €1,000 into your savings plan during that time.

In other words, compound growth would have added €483.57, almost a third of your total.

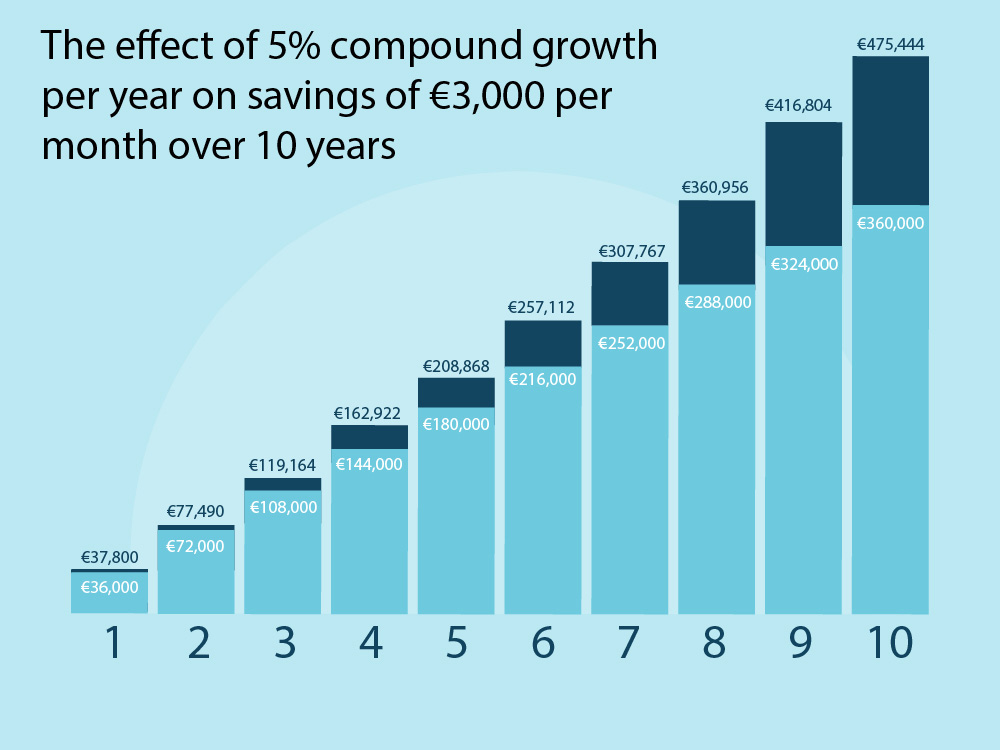

Want to know what would happen if you put €3,000 per month into a savings plan with an average annual growth rate of 5% for the next ten years?

You’d end up with…

€475,444.34

You’d almost be half a millionaire. (If you want to be an actual millionaire in this scenario, stay in yachting for 17 years and 4 months.)

By the way, during those ten years, you’d have put in €360,000. Which means compounding growth would have added €115,444.34.

Over 115k in extra money for you.

So you can see that a savings plan is far better than a savings account… but you should still have both.

The best savings strategy for superyacht crew

The best savings strategy, in our opinion, is this one.

First, save up the equivalent of 3, 6 or even 12 months’ salary. Have this available to you in a savings account.

This is your rainy day fund. You can access it immediately if you have to. This gives you peace of mind that if something goes wrong, you have the money on hand to deal with it. You’ll be able to pay your bills if you lose your job, or you’ll be able to cover a big unforeseen expense should you need to.

You do not touch this money unless you have to. It is your financial parachute. Nobody in their right mind cuts bits out of their parachute and then expects it to do its job properly when they use it.

Once you have your parachute in place, then and only then do you start thinking about putting money into a savings plan.

Because savings plans are built to give you a return on your money, you have to commit to them. As a result, you can’t always pull your money out at short notice. Nor should you want to. You want to give compound growth as much time as possible to work and earn the maximum possible for you.

Pay yourself first

A key part of your savings strategy is timing when you pay money into your savings plan.

Most people think about savings at the end of the month. They see what’s left of their salary and maybe drop that into a savings account. Frankly, the amount is either very small or nil. Who has any money left over at the end of the month?

After all, we’ve just spent the whole month paying other people: bar tenders, restaurants, coffee shops, Amazon, Netflix, Apple etc.

And if you live ashore, you also have to pay the mortgage lender or your landlord, the electricity company, the WiFi provider, the water company, the gas company, the car dealership, the tax man, your local authority, your insurance company, etc, etc.

The line of people you pay is seemingly endless.

A far better time to put money into your savings is immediately after you are paid.

In other words, you are the first person you pay by putting money into your savings.

That way, you ring fence your savings money and can feel relaxed about spending whatever is left over.

None of this means anything unless you…

Do you earn around €4,000 per month working on board a superyacht at the moment?

It’s very likely you do, or that you will soon.

Will you have €475,444.34 in 10 years’ time? Unlikely.

We don’t mean to be unkind, but the harsh reality is that most superyacht crew who have worked in the industry for 10 years or more don’t even have a fraction of that. They’ve spent every single penny.

What you have is the potential to have at least about €500,000 in 10 years’ time.

But potential is nothing without action.

If you want your €475,444.34, you’re going to have to do something.

Fortunately, it’s very easy.

Set up a savings plan. And do it sooner rather than later. Every month you wait is like stealing money from yourself.

Every year you delay just makes the theft bigger.

You have the ability to save. In fact, you have a super ability to save. Don’t waste it.

Do this today: